Newsletter November 2022:

By: Piotr Banaszek

Challenges of the foundry market in Europe in times of pandemic and war in Ukraine

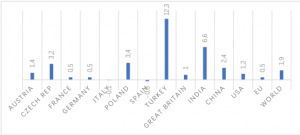

The year 2019 was very successful for the foundry industry and related industries. Unfortunately, the following year brought the COVID-19 pandemic, which stopped the development and caused a decrease in production in all branches related to casting. This decrease was felt in all European countries, and in most of them, quite drastic. China became the first country to introduce a total production blockade because of COVID-19. However, China was also the first country to return to a positive GDP result for 2020 (+ 2.4%). This year Turkey also achieved a positive GDP (+1.8%). Other countries felt the effects of the pandemic even more, and quite clearly, in the second quarter of 2020. When the lockdown was introduced in Europe, production in various industries significantly slowed down or even stopped. The year 2020 also brought a significant increase in inflation, as can be seen in Graph 1.

Graph 1. Inflation level (year to year) in selected countries of the world (and the average for the whole world) in 2020

Source: https://kimim.pan.pl/files/Sobczak_Dudek.pdf

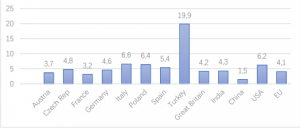

Although the end of 2020 began to bring increases in GDP in almost every country struggling with the pandemic, inflation in 2021 grew even more, as seen in Graph 2.

Graph 2. Inflation level in selected countries of the world in relation to October 2021

Source: https://kimim.pan.pl/files/Sobczak_Dudek.pdf

In 2020, the global production of castings decreased by 3,3%, i.e., around 3.6 million tons. Only a few countries increased their production compared to the previous year. The most significant decrease in the production of castings was recorded by Japan (37.4%) and Germany (29.6%), who, despite such a large decline, remained the leaders in terms of the production volume of castings (3.5 million tons) in Europe in 2020.

In 2020, iron and steel foundries of the CAEF member states (European Association of the Foundry Industry) produced a total of 9.1 million tons of castings. Compared to the previous year, this means a decrease in total production by as much as 19.8%, and the reduction of non-ferrous metal castings in CAEF member states decreased by 19.2% to 3.3 million tons in 2020. There was not a single country with CAEF which would record an increase in production in relation to the previous year. Furthermore, the ongoing pandemic has significantly reduced the number of people working in the casting industry, and some have changed to other sectors of the economy. Overall, of 130.700 employees working in foundries, around 7.5% have left work in this sector.

The increase in the costs of materials needed to produce castings is also related to increases in the costs of transport, in particular from China, where at the end of the year, freight costs from about 1,000 dollars had increased several times. For a 40-foot container between China and Europe, a significant increase in the price of scrap additives from 9.96% in December and 22.67% in January 2021 caused further disturbances in the production costs of iron castings and aluminum. Next, prices on the London Stock Exchange began to rise drastically from 1300 USD/t in May 2020 to 3000 USD/t in October of the following year (Graph3)

Graph 3. Official LME aluminum alloy prices chart

Source: https://www.lme.com/en/Metals/Non-ferrous/LME-Aluminium-Alloy#Price+graphs

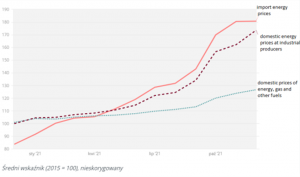

The largest drops in production were recorded by foundries that had signed contracts with companies from the automotive industry, since this industry was struggling with many other problems, such as the lack of semiconductors. They recorded in Europe a decrease in new car registrations by 24.3%, i.e. some 12 million cars less than sold a year earlier. A significant increase in steel prices due to the lack of it on the market, which was related to transport restrictions (movement bans, quarantines, etc.), along with the increase in transport prices, was significantly felt at the end of 2020. At the beginning of 2021, the situation was no better. The price of hot-rolled sheets increased by over 250% and the price of the cold-rolled sheets by about 350%, only the second quarter began to give hope for an improvement in the situation in the casting industry, and when the echoes of the ongoing pandemic began to fade away, although the prices of alloy additives were beating more records and inflation did not slow down at all, everyone expected stabilization and a return to normalcy. Unfortunately, the increase in the cost of purchase of input materials and the prices of energy carriers began to affect the profitability of production in foundries. Especially the latter problem began to be the number one topic for the profitability of production and further operations of foundries. The increase in energy costs in 2021 (Graph 4 prices in €/1mWh) was terrifying and will continue to rise in 2022, but a peak in prices is expected in 2023.

Graph 4. Energy prices in the EU 2021

Source: https://www.consilium.europa.eu/pl/infographics/energy-prices-2021/

And when all the optimistic forecasts of production increases from the beginning of 2021 and improvement in productivity for the next year began to take real shape, in February 2022, war broke out in Ukraine. On the orders of President Putin, the Russian troops attacked targets in Ukraine, the European Union, and the United States, and most countries in the world reacted by breaking trade contracts with Russia. More than 750 companies, mainly from the USA and Europe, suspended or ceased operations in Russia. The lack of supplies of metals and materials for the production of castings (ferroalloys, modifiers, nodules) caused another crisis. On the example of Poland, imports of steel products from Russia, Belarus, and Ukraine in 2021 amounted to about 3 million tons, i.e., 25% of all imports, and so Europe as a supplier becomes in the face of the shortage and rising prices of raw materials, in particular, those mined in Russia and Ukraine, necessary for many European producers:

- Lithium – production of lithium-ion batteries

- Cobalt – production of batteries and electronics

- Neon – Ukraine is one of the most important suppliers of this gas, which is used to power lasers etching patterns in semiconductors for the production of electronics (Ukrainian companies Ingas and Cryoin are responsible for about half of the world’s neon production).

- Palladium – About one-fifth of the palladium imported into Germany comes from Russia. It is used, inter alia, in the production of catalytic converters for cars.

- Nickel – Russia is an important supplier of nickel ore, which is necessary for producing lithium-ion batteries.

The European Foundry Association (CAEF) has already ruled that we have had to face such drastic price increases first time since the Second World War:

Base materials: e.g., ferrous and non-ferrous metals

Alloying elements: e.g., magnesium, silicon, copper, nickel

Chemicals and other petroleum derivatives: e.g., sand, resin, binders

Energy: e.g., gas, coke, electricity, oil

And it asks the governments of the CAEF countries to take action to help and secure the operations of foundries in this difficult time.

In the end, the closed supply corridors from Asia, and the rise in electricity and gas prices and the rise in oil prices (higher logistics costs) are problems that can be dealt with if you have the appropriate knowhow. Thanks to our many years of experience, a broad supplier base, and long-term contacts, we can support our clients to get the most favorable transport and production costs for the products they need.

Please feel free to contact us at any time. We will be happy to support you (purchasing@bdp-mc.com).